Welcome to Grupo Spurrier

Grupo Spurrier is the leading company in the provision of strategic information on economic and political issues regarding Ecuador, which we monitor through Weekly Analysis and Análisis Semanal. We specialize in economic research, competition advice, market research, business plans, and workshops in economic scenarios and regulatory changes.

Weekly Analysis Briefs

WA-2026-12: AN ART GOOD FOR 120 DAYS

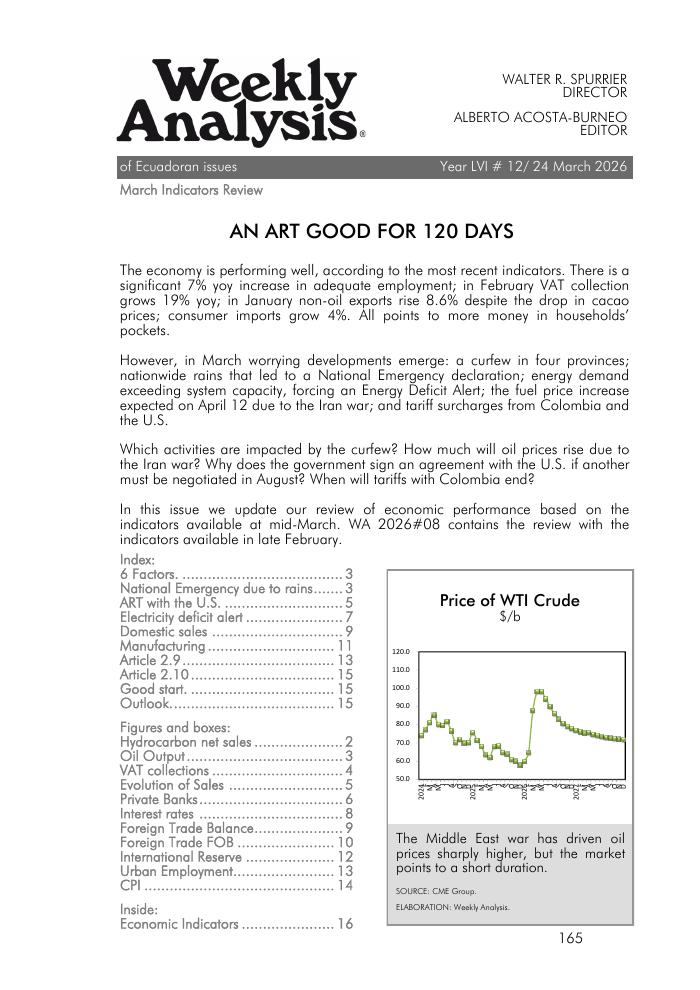

The economy is performing well, according to the most recent indicators. There is a significant 7% yoy increase in adequate employment; in February VAT collection grows 19% yoy; in January non-oil exports rise 8.6% despite the drop in cacao prices; consumer imports grow 4%. All points to more money in households’ pockets. However, in March worrying developments emerge: a curfew in four provinces; nationwide rains that led to a National Emergency declaration; energy demand exceeding system capacity, forcing an Energy Deficit Alert; the fuel price increase expected on April 12 due to the Iran war; and tariff surcharges from Colombia and the U.S. Which activities are impacted by the curfew? How much will oil prices rise due to the Iran war? Why does the government sign an agreement with the U.S. if another must be negotiated in August? When will tariffs with Colombia end? In this issue we update our review of economic performance based on the indicators available at mid-March. WA 2026#08 contains the review with the indicators available in late February.

WA-2026-11: INSURERS: A VERY GOOD YEAR

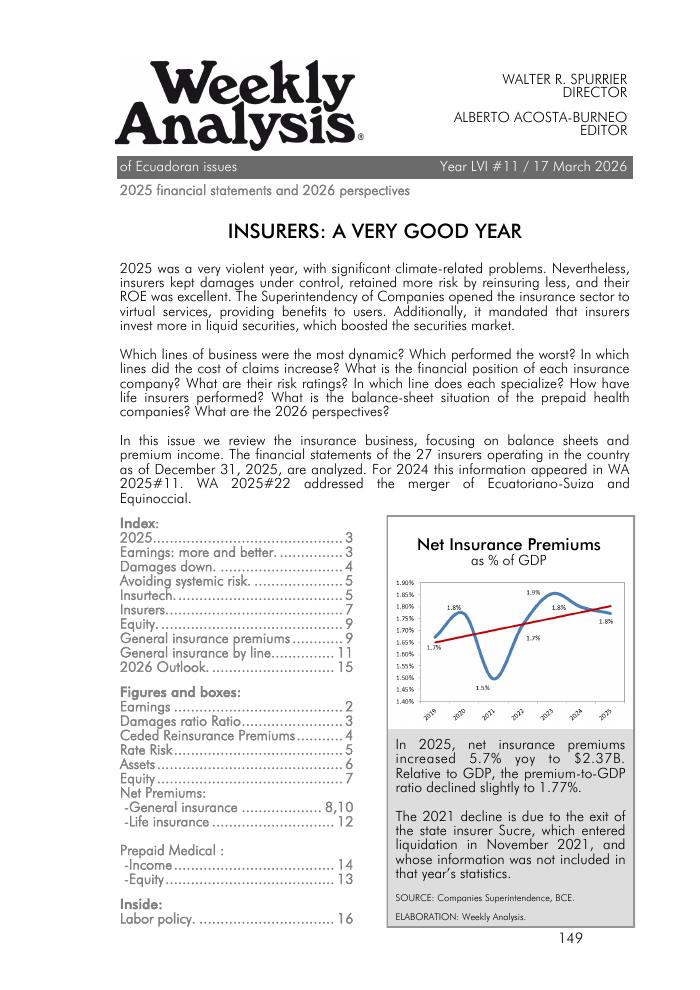

2025 was a very violent year, with significant climate-related problems. Nevertheless, insurers kept damages under control, retained more risk by reinsuring less, and their ROE was excellent. The Superintendency of Companies opened the insurance sector to virtual services, providing benefits to users. Additionally, it mandated that insurers invest more in liquid securities, which boosted the securities market. Which lines of business were the most dynamic? Which performed the worst? In which lines did the cost of claims increase? What is the financial position of each insurance company? What are their risk ratings? In which line does each specialize? How have life insurers performed? What is the balance-sheet situation of the prepaid health companies? What are the 2026 perspectives? In this issue we review the insurance business, focusing on balance sheets and premium income. The financial statements of the 27 insurers operating in the country as of December 31, 2025, are analyzed. For 2024 this information appeared in WA 2025#11. WA 2025#22 addressed the merger of Ecuatoriano-Suiza and Equinoccial.

WA-2026-10: IMPORTS FROM COLOMBIA: WHAT LIES AHEAD?

The 50% increase in Colombian tariffs has officially taken effect, a retaliatory measure following Ecuador’s own decision to raise its security rate to 50%. Ecuadoran import guilds have denounced the move, warning of the direct harm to consumers caused by rising prices. Within the industrial sector, the reaction is more nuanced: while some believe critical inputs will become drastically more expensive, others argue they can replace international supply with their own domestic production. This Friday the 13th, the ART Agreement (Agreement on Reciprocal Trade) with the U.S. will be signed. It brings a wide range of commitments for Ecuador, and on the commercial front, it grants the U.S. greater access to the national grain market, specifically for wheat and corn. What can be expected regarding Colombian imports? Which products will continue to be imported despite the high costs, and which are likely to be replaced by domestic goods? What was President Noboa’s objective at the "Shield of the Americas" Summit? Furthermore, what are the latest changes regarding courier imports?

WA-2026-09: TARIFF POKER

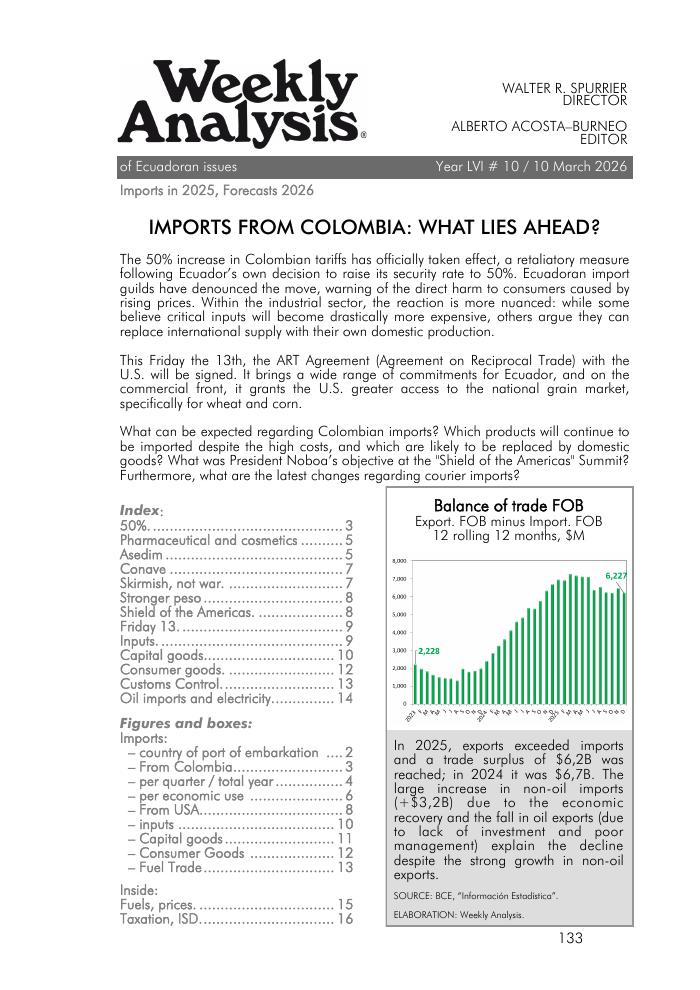

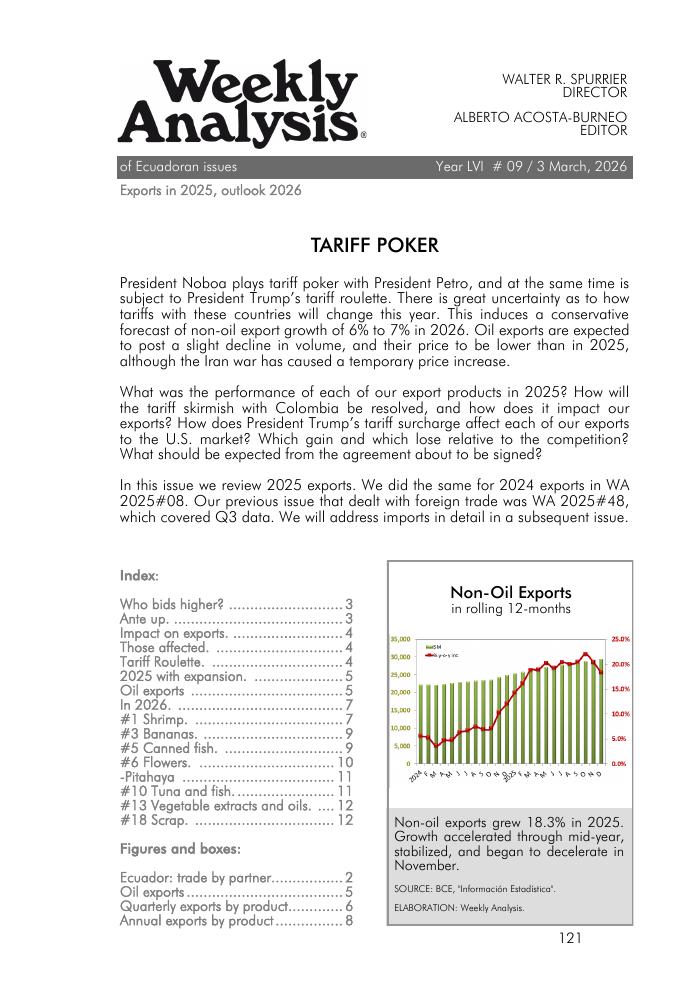

President Noboa plays tariff poker with President Petro, and at the same time is subject to President Trump’s tariff roulette. There is great uncertainty as to how tariffs with these countries will change this year. This induces a conservative forecast of non-oil export growth of 6% to 7% in 2026. Oil exports are expected to post a slight decline in volume, and their price to be lower than in 2025, although the Iran war has caused a temporary price increase. What was the performance of each of our export products in 2025? How will the tariff skirmish with Colombia be resolved, and how does it impact our exports? How does President Trump’s tariff surcharge affect each of our exports to the U.S. market? Which gain and which lose relative to the competition? What should be expected from the agreement about to be signed? In this issue we review 2025 exports. We did the same for 2024 exports in WA 2025#08. Our previous issue that dealt with foreign trade was WA 2025#48, which covered Q3 data. We will address imports in detail in a subsequent issue.

WA-2026-08: ERRATIC TARIFFS

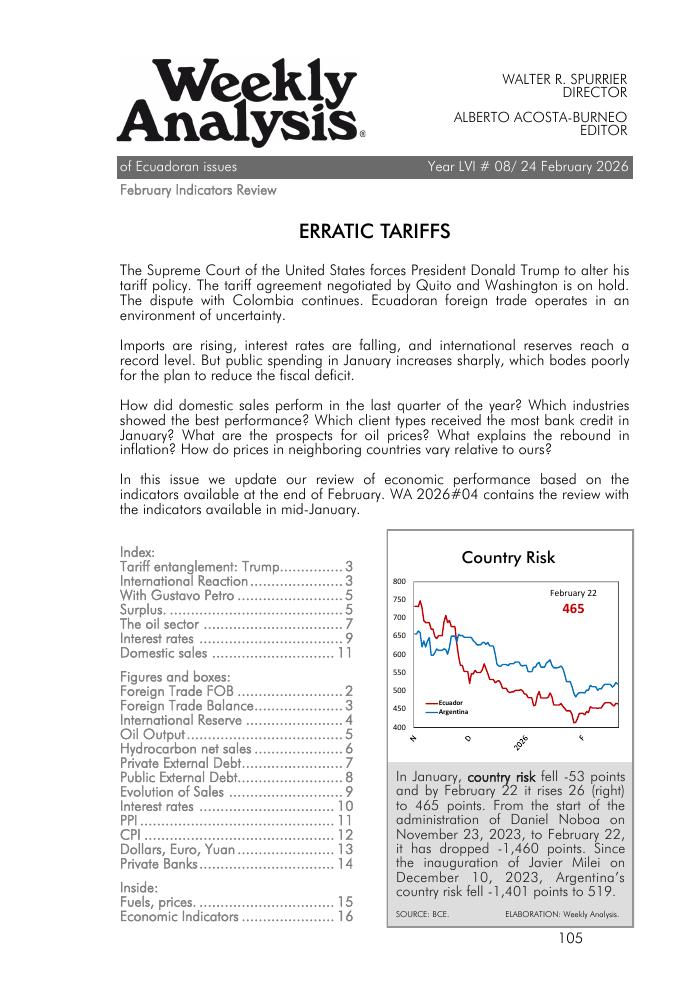

The Supreme Court of the United States forces President Donald Trump to alter his tariff policy. The tariff agreement negotiated by Quito and Washington is on hold. The dispute with Colombia continues. Ecuadoran foreign trade operates in an environment of uncertainty. Imports are rising, interest rates are falling, and international reserves reach a record level. But public spending in January increases sharply, which bodes poorly for the plan to reduce the fiscal deficit. How did domestic sales perform in the last quarter of the year? Which industries showed the best performance? Which client types received the most bank credit in January? What are the prospects for oil prices? What explains the rebound in inflation? How do prices in neighboring countries vary relative to ours? In this issue we update our review of economic performance based on the indicators available at the end of February. WA 2026#04 contains the review with the indicators available in mid-January.

WA-2026-07: STRONG CREDIT FOR 2026

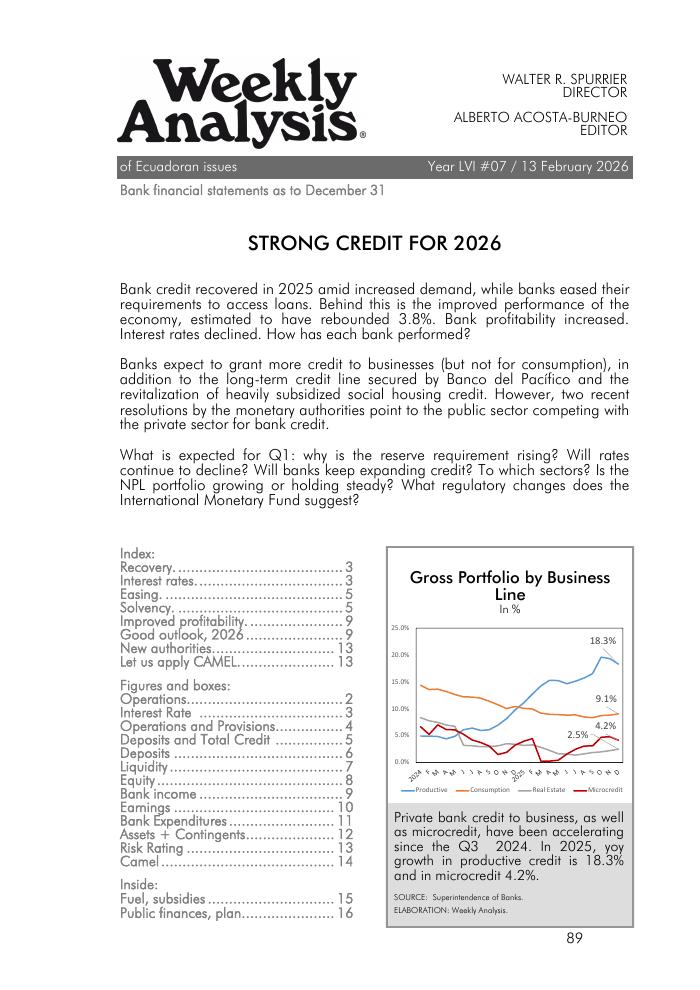

Bank credit recovered in 2025 amid increased demand, while banks eased their requirements to access loans. Behind this is the improved performance of the economy, estimated to have rebounded 3.8%. Bank profitability increased. Interest rates declined. How has each bank performed? Banks expect to grant more credit to businesses (but not for consumption), in addition to the long-term credit line secured by Banco del Pacífico and the revitalization of heavily subsidized social housing credit. However, two recent resolutions by the monetary authorities point to the public sector competing with the private sector for bank credit. What is expected for Q1: why is the reserve requirement rising? Will rates continue to decline? Will banks keep expanding credit? To which sectors? Is the NPL portfolio growing or holding steady? What regulatory changes does the International Monetary Fund suggest?